CUTTER BUSINESS TECHNOLOGY JOURNAL VOL. 30, NO. 12

Many classic change management models are not up to the challenge of guiding continuous change. Jagdish Bhandarkar and Namratha Rao observe that these models fail to consider the significant dimensions of technology and innovation. They recommend developing key performance indicators to track all dimensions of change, which will enable an organization to constantly improve its capability to implement change. Rao and Bhandarkar present a case study where a community bank “transformed the initial negative perceptions of change to a positive practice.”

The present era of digital transformation brings with it disruptive changes in technology, culture, society, economy, workplaces, and much more. In this article, we explore the problem of disruptive change by means of a case study.

We discuss the evolution of the digital change management framework (DCMF) and what we have learned from implementing changes. And we propose how to make change management more human-centric, with intrapreneurship1 opportunities and socially responsible projects that define the roadmap of short- and long-term goals of digitalization and, in the process, lay the cornerstone of empathy even within the inescapable changes happening around us.

What Is Different About the Digital Era?

Digitalization is setting new standards for industries as customers actively interact with brands and businesses online. Companies are increasingly looking to invest in digital to connect, engage, and influence their customers. Digitalization has thus paved the way for today’s all-pervasive social media.

Social media advancement has blurred the boundaries between people, with research showing that there are only “three degrees of separation” in today’s connected world. In addition, technologies like mobile, big data, and cloud have forced the digitalization of businesses across the globe. Some of the revolutionary concepts that companies are working on today include autonomous cars, robot assistance, microchips for medical purposes, gene-alteration techniques, and outer space colonization, to name a few.

Living alongside technology is a truth of this century. Thinking beyond the boundaries and equipping oneself for constant change define today’s way of life. The possibilities are infinite, and a constant paradox of thrill and paranoia exists for those imagining the future. This is what separates this era from previous generations.

Disruption is a superlative degree of change. The new normal that emerges is perceived to appear in a blink of the eye. In such a situation, when is the right time to respond to such a change? Is the company equipped to transform itself and compete with the first movers2? Or is catching up the only way to survive? Can disruption be an inside-out change? Can a company visualize its own value curve3 and carve a blue ocean,4 hence becoming the harbinger of disruption itself?

Whatever the path to survival in today’s digital era, what has worked before will not work for the future. Companies must continuously innovate and, throughout this process, must manage changes effectively to realize the value of innovation. The constant pace of innovation could mean that the classic change management techniques are no longer valid.

Changing Course

Most current change management models advocate the typical cycle of assessing the need for change, planning steps to make the change, communicating the change, implementing the change, and tracking progress to sustain the change. While frameworks like the Deming Cycle (aka PDSA — Plan, Do, Study, Act) and the EASIER (Envision, Activate, Support, Implement, Ensure, Recognize) model are operational in nature, models like Prosci ADKAR are oriented toward a singular view of individual change management, and others, like the McKinsey 7S Framework, are too complex for large organizations to follow.

Years of slow change or overconfidence as to current success could make a company intrinsically less prepared to handle the disruptions happening today. The decline of companies like Blockbuster or Kodak are classic examples. Change management boards, which in theory must be fluid and responsive, may be incapable of identifying the sense of urgency and hence unprepared to manage the rapid changes happening around them.

Evolution of the DCMF

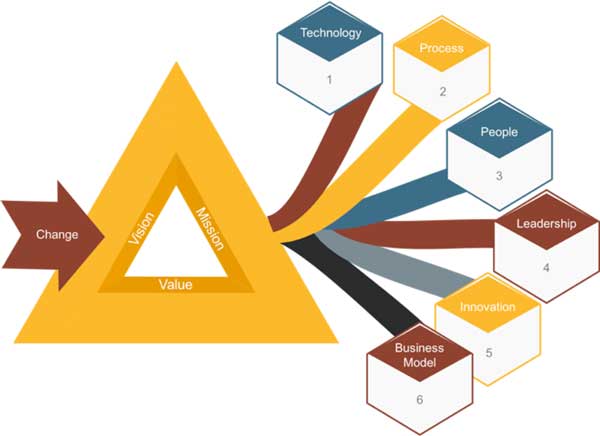

Endowing the old change management frameworks with the additional dimensions of technology and innovation could help change a company’s course. Along with process, people, leadership, and business, a new-age DCMF should emphasize developments in technology and innovation as well (see Figure 1). When change is assessed, the complexities of this change appear in the form of the dimensions illustrated in the spectrum in Figure 1. These are a company’s most significant dynamic variables affecting the implementation of digital change.

The application of the classic change management technique of assess-plan-implement-track to the dimensions of the digital change management spectrum produces the DCMF, which companies can use to manage digitalization. Change management needs to assess all these dimensions to evaluate the impact of a change. Key performance indicators (KPIs) and benchmarks must be set for each dimension of the spectrum to govern the overall effort and risk and to ensure successful change implementation.

As an example, agility-related KPIs need to be mandatory for each dimension. KPIs such as swift decision-making leadership and a flexible business model can be the pillars of support that an organization needs. Other KPIs measure technology maturity and associated skills, degree of knowledge sharing and collaboration, creative processes that enable harnessing the collective abilities of the organization, and so on.

A vital dimension of the spectrum is innovation, which defines how capable an organization is to lead a change or even play catch-up. A culture of rapid ideation and co-creation can jump-start certain initiatives and can be measured. Table 1 provides sample KPIs for the technology dimension.

The result of any change, whether inside-out (a company-initiated change) or outside-in (an

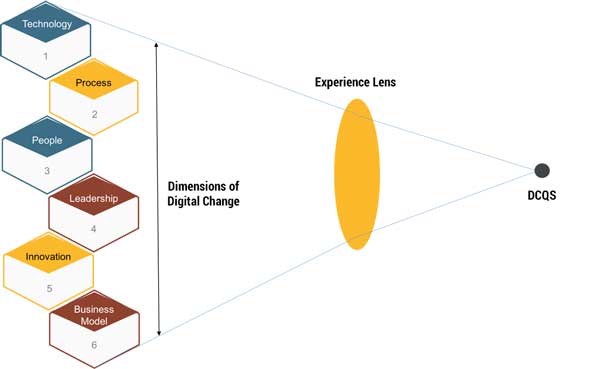

outside-imposed change), can be modeled to represent customer and employee experience. Customers and employees can be surveyed about their post-change experiences, and a digital change quotient score (DCQS) can be calculated by examining the results of the survey. Figure 2 illustrates how the dimensions of the spectrum can be viewed through the “experience lens” of customers and employees to predict the DCQS.

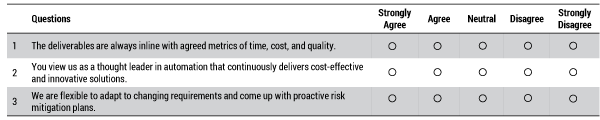

The sample customer survey shown in Figure 3a includes questions related to compliance to the agreed terms for project deliverables, along with the innovation and flexibility exhibited in that time frame. Qualitative feedback can also be sought from customers.

As shown in the sample in Figure 3b, an employee survey might include questions related to employee experience in bringing about a change and employees’ general outlook for the company.

Each survey question is assigned an experiential weightage between 0 and 1 (a percentage value to prioritize the responses based on the type of change exercise being undertaken). This weightage is multiplied with the five-point-scale survey result. The customer and employee surveys are scored accordingly. The DCQS is an average of the sum of scores of both these surveys on a five-point scale. A company’s DCQS indicates its capability to successfully deliver change. This score can be improved over time by applying lessons learned techniques.

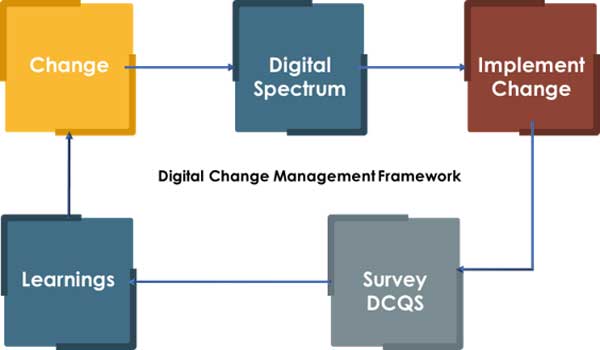

By deconstructing both success and failure stories and learning what to repeat, what to avoid, and what to do differently, this indicator can serve as a reference point that companies can use to constantly improve. A company’s DCQS can also bring a degree of predictability into its change management process. When tracked continuously, this indicator — and hence the framework — can transform change into a habit, thereby making change less painful. Figure 4 shows the DCMF in action.

Leadership and Change

Today, every company is viewed as a technology company. Customers expect a digital experience, so companies are moving to digitalize their approaches toward services, operating models, and products. Nike, Netflix, and Amazon are examples of companies where digitalization has brought about massive changes not just in the technology used but also in value chains, organizational structures, operational processes, and revenue models.

The path to becoming a digital company is difficult and the challenges are multifold. It means ensuring customers remain connected even with the drastic changes that may be needed and overcoming resistance to new business models. Becoming digital does not simply mean implementing new technology; it also requires developing new leadership skills combined with connectivity among a company’s people, processes, and data. Cultural changes may also be a challenge if the digital transformation must cut across silos in the organization.

Driving Change: A Case Study

The word “banking” may conjure an image of a large corporate entity with millions of dollars in assets spread out across the globe. Yet among these players are fintech startups like GreenSky and Stripe, which have emerged with new technological innovations and have become potential threats to traditional financial institutions. Due to such competition to become sustainable digital entities, large banks have invested millions of dollars.

But community banks constitute a portion of banking institutions as well and are part of the fabric of smaller communities. These banks have neither the major assets nor the investments of large banks, nor the financial and technical agility of fintechs. What community banks do have is a loyal customer base and community support. For community banks, implementing innovative technology is excessively costly and switching to a digital track is a challenge.

Our case study examines the implementation of a digital change in a US community bank meant to retain its loyal customer base and to put in place newer ways of monetization. The bank’s newly named CEO brought with him years of experience in applying digital in the banking world. His first quest at the community bank was to understand customer expectations and to assess how the bank performed and what needed to be changed.

Among the bank’s retail customers, the younger generation wanted around-the-clock availability of services, while the older generation preferred to visit branches and would tolerate the accompanying delays. For commercial customers, the lack of remote depositing of checks was causing them to shift their accounts to bigger banks. That service feature would be one of the core blocks of the bank’s digital transformation.

With the US Check Clearing for the 21st Century Act (Check 21), trips to a local branch or lockbox site to deposit checks had become a thing of the past for many US corporations. The combination of Check 21 legislation and advances in check imaging technology provided the ability to automate the deposit process, adding significant value to corporate treasury operations. Moreover, remote deposit capture (RDC) emerged as a popular method for automation of the deposit process driven by advances in check electronification.

Apart from other expectations, the community bank’s commercial customers were demanding the availability of RDC, which would allow them to set their own operational timelines without needing to adhere to the bank’s constraints. Commercial establishments needed this ability to manage costs associated with the processing of paper checks and to lower transportation costs by reducing or eliminating trips to the bank.

The CEO communicated these commercial customers’ expectations to the bank’s employees. On the one hand, employees immediately perceived the RDC change as likely to result in a change in the number of days and hours worked and possibly the elimination of jobs. On the other hand, the advantage to the bank would be considerable, as there would be no need for the higher-volume operations in checks that incurred significantly higher time and cost.

The CEO faced three challenges in implementing this change: (1) taking care of customer expectations was the priority; (2) letting employees go would mean abandoning the bank’s community roots and mission and was therefore not an option; and (3) implementing the technology changes required would incur significant investment.

The CEO took the decision to move to digital; newer models would help the bank face its challenges. To assist in this change process, the bank hired a change management consultant and insisted on a plan for future self-sufficiency. The consultant’s responsibilities were to add value during the assessment and planning process, to educate the board, and, during the early days of the project, to help organize and accelerate the change process, bringing experience and helping the bank avoid mistakes other organizations had made.

The introduction of the DCMF allowed the CEO to look at the bank’s problems through the dimensions of people, technology, innovation, business model, process, and leadership. The DCMF also emphasizes communication, both to internal and external entities, and the bank’s new mission and renewed vision were made clear to employees and customers. The classic change management processes of assess-plan-implement-track were applied to every dimension of the digital change management spectrum.

The bank clearly outlined the business benefits to its commercial customers that would come out of the changes to its business model from implementing RDC: accelerated clearings, improved cash management operations, bank treasury consolidation, reduced transportation costs, and time savings. The benefits for the bank from the change to its business model included reduced transportation costs in areas like ATM deposit pickups, branch cost savings, and a smaller number of incoming customer cash letter deposits. The CEO also noted that RDC can open doors for new revenue streams by the addition of new clients and making possible a larger wallet share with existing clients, as well as the utilization of additional products that arise from RDC, such as ACH (Automated Clearing House) transactions, checks, liquidity services, and so on.

The challenge for the technology aspect was to create an integrated receivable platform that would accept, process, and post any payment method from any payment channel. The CEO initiated a technology portfolio discussion with his lines of business (LOBs) and IT leads to draw up an IT strategy. Prior to the CEO’s tenure, IT determined which products to buy off the shelf and which to build from scratch. The culture now changed to LOBs funding IT, and thus making a joint informed decision. This reduced friction between the LOBs and IT in the bank’s digital journey and paved the way for the creation of a full-fledged support model. The LOBs used this support model to address customer queries or issues, and IT employees now realized the importance of the IT strategy in delivering the promised value to customers and began to empathize with customers and with LOB colleagues who were having to interact with customers in the event of any downtimes.

The benefits came with associated risks. Those risks centered around who should be using the RDC feature and how the bank would monitor the associated RDC account risk. A risk assessment presented to the CEO and the board helped in setting up a formal risk review process and mitigation procedures. The LOBs and IT used the risk review findings to effect changes in the process the LOBs followed and in the technology IT handled. This was done iteratively so that the bank can be comfortably situated when audited by the US Federal Reserve System.

The people dimension provided the CEO with his most important challenge, and one that had to be handled with extreme care. He brought with him not only years of banking experience, but also a philosophy and deeply held set of principles about how to be an effective leader. The CEO conveyed his belief that digital transformation should be a strategic imperative set out to recruit and employ the “right people,” as well as focusing on training and developing his entire team. The bank already had most of the people and talent needed and required minimal additional recruiting.

The CEO built a digital transformation group that included the consultant, along with key associates in the LOBs and IT departments. The digital transformation group also took stock of the existing employees and their interests to develop cross-training plans if some jobs were eliminated and to ensure that the community was not harmed due to the bank’s digital route. The group also inculcated the importance of pulling together a cross-departmental team that would go beyond IT and operations. It held the core belief that the customer experience — and not the technology — was of prime importance. Implementation of a strong succession plan helped ensure that the bank would continue to provide high-quality relationship management, a service its customers appreciated.

The board and the community were iteratively briefed on the digital transformation process as part of the transparent communication initiative. Their satisfaction with the communication and the process helped the CEO obtain the additional funding necessary to cement his vision to make the bank more digitally oriented.

The CEO also worked on engaging the community and creating positive PR for the bank. Beyond the typical helping hand for local organizations, the bank developed an innovative initiative to involve the community in the bank’s improvement through an idea-generation portal. Any community member could use the portal to suggest an idea that might help the bank — anything from how to improve the execution of initiatives to a strategy for deciding on new initiatives. The community member who contributed an accepted suggestion and problem solution became the champion from the community to oversee the completion of that solution. The idea-generation portal gave the community faith in the bank’s leadership.

Assessing the changes required for each dimension of the DCMF resulted in a set of KPIs to track. Customers welcomed the RDC service and employees were satisfied with the painless implementation of the digital strategy. Employees and customers were surveyed to determine the DCQS. Once the score was known, the digital transformation team worked to resolve any issues at each dimension of the spectrum, ensuring that the KPIs were adhered to and were effectively captured and measured.

The continuous improvement attitude inherent in the DCQS has fostered a culture of innovation and planning for what is ahead for the bank. As a next phase, the bank is now evaluating the means of applying analytics and predictions to its customers and is ready to roll out the change. Focusing on each dimension of change and quantifying the results of implementation have transformed the initial negative perceptions of change to a positive practice in the bank.

Human-Centric Approach to Rapid and Disruptive Changes

Disruptive changes within a company can result either in a spectacular rise if done right or an abrupt decline if not handled well. People are at the center of every change. If employees do not connect with their organization, do not see the need for change, do not buy in to the leadership’s vision, or are not motivated, any change will fail.

For employees to see value beyond the defined work parameters, they need to feel connected to the company. In a world of frequently changing loyalties, companies must focus on engaging their people at a very basic level. Respect and trust can be built by showcasing in earnest the company’s initiatives toward the greater good. Connection, respect, and trust will help a company maintain employee support for the changes that a company wants to implement.

Below, we discuss in brief two such initiatives that brought about drastic increases in employee support and participation.

Initiative 1: The Social Responsibility Factor

When a Fortune 500 company conducted an employee satisfaction survey, it became clear that the employees were not highly connected to the company’s vision and were only moderately motivated at work. While there were many takeaways from the analysis of the results, a few key issues were considered attributable to insufficient employee engagement:

-

General sense of detachment from the success or failure of the company’s initiatives

-

Neutral outlook on the company’s leadership

-

Insufficient pride in the company’s brand

These takeaways explained to an extent why employees were not meeting each change initiative the company took on with enthusiasm and a sense of ownership.

One key initiative close to the CEO’s heart was her contributions toward corporate social responsibility. A select few ran such projects. Despite communication about these projects, employees did not identify with them. After some deliberation, the leadership team decided to open these projects to all employees. They were, for example, invited to participate in an activity that aimed to donate food and clothing to a flood-stricken area in a neighboring state. Many employees at all levels became involved, and the project brought the company’s people together.

This experiment reaffirmed the idea that, when a company’s people connect with each other and see the company’s leadership as responsible and trustworthy, a sense of belonging naturally occurs. Having built and nurtured such an environment, the company now finds it comparatively easy to engage employees and drive change.

Initiative 2: Intrapreneurship Opportunities

A Fortune 100 company was quite successful in driving change and outperforming its competitors. But leaders observed that it was only the team dedicated to R&D that was quickly implementing changes to catch up with industry trends. So the leadership asked middle management to come up with possible solutions. Within a few days, middle management had suggested several ways to solve this problem, including one that was unique: intrapreneurship.

The goal was to create an environment in the company conducive to innovation and research. Creative ideas likely to result in a business win or revenue-generating opportunities were given the necessary hearing and then funding by the “idea board,” which comprised important company stakeholders. The idea generators, called “intrapreneurs,” owned the project and received a percentage of the revenue generated by the project upon realization. This resulted in enhancing the feeling of ownership, accountability, responsibility, and involvement of the people who participated in such projects.

Intrapreneurship acted as a sounding board for employees, who generated ideas that became real differentiators for the company. The company saw an increase in curiosity to think out of the box, to be aware of what is happening in the world today, and of how to apply certain concepts for the benefit of the company.

Change Is Imminent

Both social responsibility and intrapreneurship show that by taking a human-centric approach, involving people, and winning their loyalty, it becomes easier to identify and drive tough changes within a company. Change is the only constant. In today’s digitalized world, the only thing any company can predict with 100% certainty is that change is imminent.

Preparedness is the best bet for a company to survive in these tumultuous times. By effectively employing the dimensions of the DCMF, leaders can be the anchors of change. Our case study shows that in the digital era, every company — small or big — can be a change maker and create a difference by embracing the advantages that digital brings. When leaders gain employee trust and enhance engagement with intrapreneurship and involvement in social responsibility initiatives, employees are more favorable to change. People come to expect change rather than seeing it as a surprise or, more often, a shock. Slowly, this thought process becomes the norm and is internalized into the genetics of the organization.

1 An intrapreneur is a person who behaves like an entrepreneur while being employed, developing an idea into a workable product for the company he or she works for.

2 ”First mover” refers to a company that gains competitive advantage by being the first to bring a product or a service to a market.

3 ”Value curve” is a depiction of a company’s relative performance across its industry’s factors of competition.

4 A “blue ocean” is a new, uncontested market space that, when created, makes the competition irrelevant. For more on blue ocean, see Blue Ocean Strategy: How to Create Uncontested Market Space and Make the Competition Irrelevant.